Get In-Demand Finance Certifications

As an FP&A analyst, examining variances between forecasts and actuals is central to your role. What many new analysts miss is strategic insight. In addition to technical proficiency, knowing how to approach variance analysis strategically helps businesses plan better, allocate resources wisely, and manage risk.

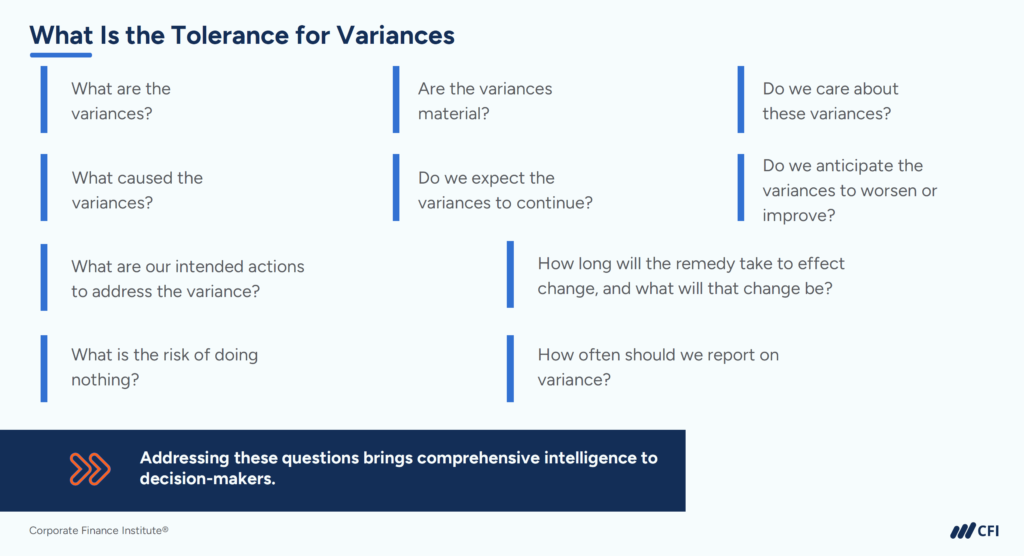

The 10-question framework presented below can help you move beyond basic calculations to deliver meaningful business insights. Whether you’re new to variance analysis or looking to sharpen your approach, this framework will help you ask smarter questions and uncover deeper insights.

Sometimes you’ll have high confidence in your forecasts, and the results will affirm your assumptions. Other times, despite careful planning, the actual results will surprise you. This is normal and expected. As the saying goes, “When you fail to plan, you’re planning to fail.”

The value lies not in perfect accuracy, but in the insights you gain from understanding why variances occur and what they mean for the business. Meaningful variance analysis goes far beyond calculating differences — it’s about understanding the story behind the numbers and their implications for your business.

To help you develop deeper insights, follow the 10-question framework to develop deeper insights that add tangible value.

Start with the basics but be strategic. Focus on identifying significant variations in key business drivers and metrics. For example, if you’re analyzing sales performance, look beyond the total revenue variance to understand differences in volume, price, and mix.

| Quick Tip

Always calculate both absolute ($) and percentage (%) variances to get a complete picture. |

⚠️ Common Pitfall

Getting lost in calculating every possible variance instead of focusing on key metrics that drive business performance. |

Not every difference requires action. Consider both absolute dollar amounts and percentages. A $50,000 variance in office supplies might be less concerning than a $50,000 variance in direct materials, even though the numbers are identical.

| Quick Tip

Establish materiality thresholds for different expense categories based on their strategic importance. |

⚠️ Common Pitfall

Treating all variances of the same size equally without considering their context. |

| Pro Tip: Create a simple materiality matrix that maps variance sizes to required actions based on the account type. | |

This question helps prioritize your analysis. A 2% variance in material costs is likely more important than an 8% variance in cell phone expenses, especially when material costs are a key driver of business performance. Focus on variances that impact strategic decisions or indicate potential problems.

| Quick Tip

Align your variance analysis priorities with your company’s key performance indicators (KPIs). |

⚠️ Common Pitfall

Spending too much time analyzing variances that don’t impact strategic decision-making. |

Dig deep into root causes. Consider both internal and external factors. For example, a revenue shortfall might result from lower sales volume (internal) or unexpected competitor actions (external). Understanding causation helps inform corrective actions.

| Quick Tip

Use the “5 Whys” technique to get to the root cause of significant variances. |

⚠️ Common Pitfall

Accepting the first explanation without investigating deeper underlying causes. |

| Pro Tip: Create a cause-and-effect diagram for complex variances to visualize potential contributing factors. | |

Some variances are one-time events, while others signal ongoing trends. A missed customer payment causing a temporary cash flow variance is different from a sustained increase in raw material costs. Your response should vary accordingly.

| Quick Tip

Plot variance trends over time to distinguish between one-off events and emerging patterns. |

⚠️ Common Pitfall

Overreacting to temporary variances or underreacting to systematic ones. |

Look forward, not just backward. If a variance is trending in the wrong direction, early intervention might be crucial. Consider creating sensitivity analyses to model potential future impacts.

| Quick Tip

Create simple scenario models to project how variances might evolve under different conditions. |

⚠️ Common Pitfall

Focusing solely on historical trends without considering future market conditions or business changes. |

| Pro Tip: Develop a simple tracking dashboard that flags accelerating negative trends for immediate attention. | |

Develop specific, actionable recommendations. Instead of simply noting that costs are too high, propose targeted solutions, such as “We can reduce material costs by 5% by consolidating suppliers and negotiating volume discounts.”

| Quick Tip

Always pair variance findings with at least one specific, measurable recommendation. |

⚠️ Common Pitfall

Providing vague recommendations like “improve efficiency” without specific action steps. |

Be realistic about timelines. Some fixes, like adjusting pricing, might show immediate results. Others, like implementing new processes or systems, require longer-term planning and monitoring.

| Quick Tip

Break down remediation plans into short-term actions and long-term solutions. |

⚠️ Common Pitfall

Setting unrealistic timeline expectations that can’t be met with available resources. |

| Pro Tip: Create a timeline visualization showing key milestones and expected impact dates for major variance corrections. | |

Match reporting frequency to the nature of the variance and its importance. Critical operational metrics might need daily monitoring, while others can be reviewed monthly or quarterly.

| Quick Tip

Align reporting frequency with the time needed to implement meaningful changes. |

⚠️ Common Pitfall

Over-reporting minor variances or under-reporting critical ones. |

Always consider the consequences of inaction. Sometimes, the cost of fixing a variance might exceed the benefit. Other times, small variances might signal bigger problems that require immediate attention.

| Quick Tip

Quantify the potential financial impact of not addressing the variance over different time horizons. |

⚠️ Common Pitfall

Overlooking compounding effects that can turn small variances into major issues over time. |

| Pro Tip: Develop a simple risk assessment matrix that weighs the cost of action against the cost of inaction. | |

These ten questions form a comprehensive framework for analyzing budget variances, but remember — the goal isn’t to mechanically work through each question. Instead, use this framework as a guide to develop deeper insights about your business’s performance.

While some variances may only require a few of these questions to reach a conclusion, others might need you to explore all ten in detail. The key is to remain flexible and adapt your analysis to the specific context of each situation.

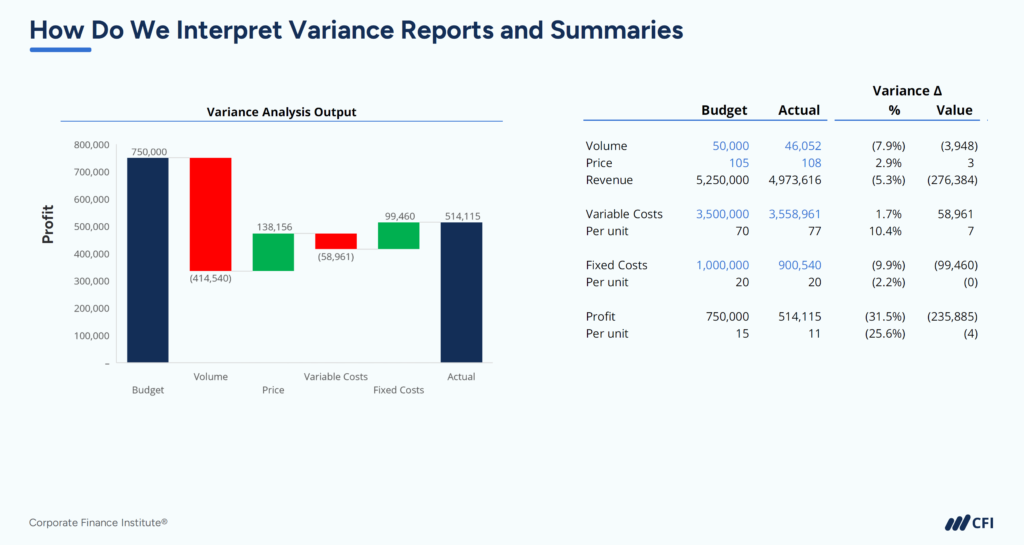

Let’s see how these questions work in a real scenario. Imagine you’re analyzing a manufacturing company’s Q1 results and discover that material costs are 8% above budget. We will use the results data in the image below to analyze this material cost variance.

Let’s see how these questions work in a real scenario. Imagine you’re analyzing a manufacturing company’s Q1 results and discover that material costs are 8% above budget.

| ✅ Initial Analysis | 1. What is the variance? | $414,540 unfavorable variance |

| 2. Is the variance material? | Material difference from budget confirmed | |

| 3. Do we care about the variance? | Significant — materials are key cost driver | |

| ✅ Root Cause & Impact | 4. What caused the variance? | • Volume changes • Price increases |

| 5. Do we expect the variance to continue? | Price increases appear permanent | |

| 6. Do we anticipate it will worsen or improve? | Further cost increases likely with volume growth | |

| ✅ Action Planning | 7. What will do about the variance? | • Negotiate new supplier contracts • Explore alternative materials |

| 8. How long will the remedy take? | 3-6 months for new supplier agreements | |

| 9. How often should we report on the variance? | • Weekly cost tracking • Monthly supplier reviews |

|

| 10. What is the risk of doing nothing? | 2-3 percentage point annual margin erosion if no action taken |

Remember, effective variance analysis isn’t just about identifying differences — it’s about driving better business decisions. By consistently applying these ten questions to your variance analyses, you’ll develop deeper insights and more actionable recommendations.

Understanding how to analyze budget variances effectively is a crucial steppingstone in your FP&A career. Consistently applying these ten essential questions shifts your focus from merely identifying variances to telling the story behind them and guiding strategic decision-making.

Ready to take the next step in your FP&A career journey? Master KPI-driven decision-making with CFI’s FP&A Specialization. Whether you’re new to FP&A or advancing your career, this program equips you to use KPIs, budgets, forecasts, and financial models to thrive in this in-demand role.

KPIs in FP&A: Measuring What Matters Most